Why Banks Are Replacing Legacy CRMs for Omni-Channel Relationship Insight

Why Banks Are Replacing Legacy CRMs for Omni-Channel Relationship Insight December 19, 2025 11:56 am Adil Gouri Why Banks Are Replacing Legacy CRMs for Omni-Channel Relationship Insight Banks aren’t losing customers because their products are weak—they’re losing relevance because they don’t recognize customers consistently across channels. A relationship that starts in a mobile app, pauses at a call center, and resumes at a branch often feels like three separate conversations. For customers, that gap feels careless. For banks, it’s a warning sign that legacy CRM systems are no longer keeping up with how relationships actually work today. Across BFSI, the operating environment has shifted fast. Customers expect real-time responses, personalized offers, and frictionless service—whether they’re applying for a loan online, chatting with support, or walking into a branch. At the same time, banks are juggling strict regulatory controls, data residency requirements, and rising competition from digital-first players who design experiences around data, not departments. Relationship insight has moved from a “nice to have” to a core differentiator. The problem is that most legacy CRMs were never designed for this level of orchestration. They store data in product-centric silos, rely heavily on manual updates, and struggle to ingest signals from modern channels like mobile apps, chat, email, and third-party platforms. Relationship managers see partial profiles, service teams lack transaction context, and marketing operates on outdated segments. The result is missed opportunities, inconsistent service, and increased operational friction—all while customer expectations keep rising. This is where banks are rethinking CRM architecture entirely. Platforms like Salesforce shift the model from static records to a unified relationship layer. Customer 360 capabilities consolidate data across accounts, transactions, service interactions, and digital touchpoints into a single, real-time view. APIs and integration layers—often powered by MuleSoft—connect core banking systems, payment platforms, and external data sources without compromising security or compliance. Built-in role-based access, encryption, and audit controls help banks meet regulatory obligations while still enabling agility. Consider a mid-sized retail bank modernizing its relationship management. Previously, a customer upgrading from savings to wealth products required manual handoffs between teams, duplicated data entry, and follow-up calls to revalidate information. After moving to an omni-channel CRM model, customer activity from mobile apps, branch visits, and service tickets flowed into one profile. Relationship managers could see intent signals early, service agents resolved issues with full context, and offers were triggered automatically based on behavior—not guesswork. The benefits go beyond better visibility. Banks see faster response times, higher cross-sell conversion, reduced manual effort, and more consistent compliance reporting. More importantly, teams begin operating around the customer rather than around systems. Decisions become data-driven, interactions feel intentional, and trust improves—an outcome that’s hard to quantify but critical in financial services. Looking ahead, omni-channel insight will only deepen. AI-driven recommendations, predictive service alerts, and automated compliance checks are becoming standard expectations, not future aspirations. Salesforce’s continued investment in Einstein AI, industry data models, and financial services accelerators positions banks to scale personalization without increasing risk. The CRM is no longer just a system of record—it’s becoming a system of intelligence. If your organization is evaluating how to move beyond legacy CRM limitations, the conversation shouldn’t start with features—it should start with relationship maturity. We help banks assess their current state, design secure omni-channel architectures, and turn CRM investments into measurable relationship outcomes that last. Latest Post 19Dec BlogsRetail Why Banks Are Replacing Legacy… Why Banks Are Replacing Legacy CRMs for Omni-Channel Relationship Insight December 19, 2025 11:54 am… 15Dec BlogsRetail Loyalty 3.0: Salesforce’s Predictive Personalization… Loyalty 3.0: Salesforce’s Predictive Personalization Shift in Retail December 15, 2025 2:41 pm Darpan Karanje… 11Dec BlogsUtility How Salesforce Drives Lean Manufacturing… How Salesforce Drives Lean Manufacturing & Waste Reduction December 11, 2025 10:30 am Aadinath Magar…

Is the Branchless Bank the Future? How Salesforce Will Enable Fully Digital Banking by 2030

Is the Branchless Bank the Future? How Salesforce Will Enable Fully Digital Banking by 2030 Is the Branchless Bank the Future? How Salesforce Will Enable Fully Digital Banking by 2030 November 27, 2025 8:00 am Laxman Gore Banks aren’t asking whether customers want digital anymore—the real question is how long physical branches will remain relevant. As consumer expectations shift toward instant, app-driven interactions, the idea of a branchless bank is quickly moving from innovation to inevitability. Yet behind the scenes, most financial institutions are still wrestling with legacy stacks, complex compliance demands, and siloed data models that make this shift harder than it sounds. The finance industry sits at an inflection point. Neo-banks are setting a new baseline for experience: onboarding in minutes, conversational service, predictive insights, and 24/7 access without stepping into a branch. Meanwhile, traditional institutions face cost pressure, margin compression, and rising regulatory scrutiny. Digitization is no longer about convenience—it’s about survival, scalability, and trust. The winners will be those that modernize their core while building operational agility across every customer touchpoint. But the path to a fully digital model is still constrained by fragmented systems, manual KYC/AML processes, disconnected service channels, and product teams that can’t move as fast as the market demands. Banks want real-time visibility, but core systems keep data locked away. They need hyper-personalized engagement, but legacy CRMs still function like filing cabinets. Most importantly, they want to scale digital operations without compromising compliance—a challenge that traditional architectures weren’t designed to solve. This is where Salesforce is quietly redefining the blueprint for digital banking. Across Financial Services Cloud, Experience Cloud, and Einstein AI, the platform is becoming the connective tissue unifying customer profiles, compliance workflows, service operations, and product origination. Instead of trying to rip out decades-old cores, banks are increasingly using Salesforce as the orchestration layer—centralizing customer data, standardizing processes, integrating KYC/AML engines, and powering multi-channel digital experiences. For an industry leaning toward branchless models, this orchestration is the difference between truly digital and simply “paperless.” Consider a retail bank aiming to eliminate 60% of its physical branches by 2030. Today, account opening might involve multiple handoffs, offline documents, and verification delays. With Salesforce, the bank could shift to a digital-first flow: customers begin onboarding through an Experience Cloud portal; identity verification happens through embedded API integrations; advisors get a unified 360° profile to validate risk through Financial Services Cloud; AI flags anomalies in real time; service reps see the full context if a customer needs help mid-onboarding. The result is a cohesive, end-to-end digital journey that feels effortless to the customer and compliant to the institution. The operational impact is massive. Digital origination cycles accelerate from days to minutes. Service costs drop as AI-driven self-service and proactive alerts replace branch traffic. Risk teams get cleaner data and automated compliance checks, reducing errors and manual reviews. Marketing teams can personalize offers based on life events, behaviors, and financial health scores powered by Einstein AI. And leadership gains a real-time view of customer engagement, profitability, and experience trends—something that is nearly impossible with traditional siloed systems. Looking ahead to 2030, the financial institutions that thrive will be those that move beyond digitizing individual processes and instead architect a unified experience ecosystem. AI will guide financial decisions, embedded finance will blur boundaries between industries, and branchless models will become mainstream. Salesforce’s evolving capabilities—from real-time data harmonization to AI-powered decisioning—position it as a foundational layer for banks entering this new era of digital-only operations. If you’re evaluating how Salesforce fits into your digital banking roadmap, we help organizations build the right architecture, define transformation priorities, and translate CRM investment into measurable financial outcomes. Latest Post 27Nov BlogsUtility How Salesforce’s Renewable Energy Commitments… How Salesforce’s Renewable Energy Commitments are Reshaping Corporate Clean Power Procurement November 27, 2025 10:09… 27Nov BlogsHealthCare Leveraging AI & predictive analytics… Leveraging AI & predictive analytics to move from reactive treatment to predictive treatment November 27,… BlogsFinancial ServiceHealthCare Is the Branchless Bank the… Is the Branchless Bank the Future? How Salesforce Will Enable Fully Digital Banking by 2030…

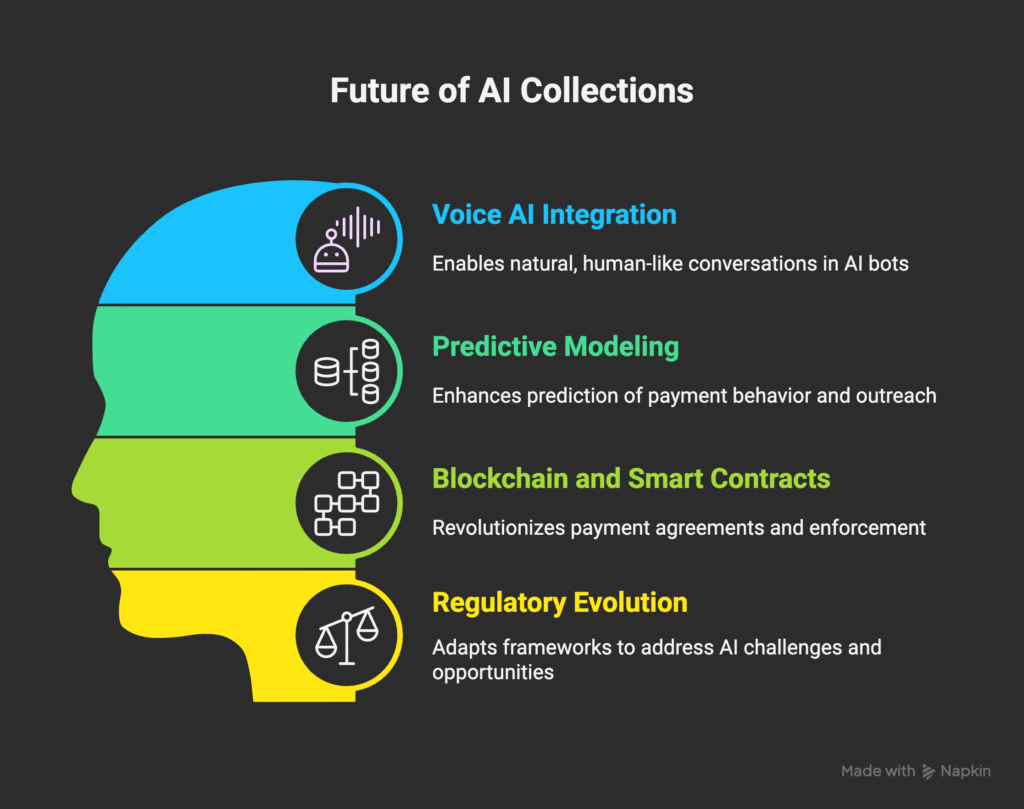

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections The collections industry is experiencing a seismic shift. While most organizations still rely on human agents making countless phone calls, forward-thinking companies are deploying AI-powered bots that integrate seamlessly with WhatsApp and Salesforce CRM triggers, achieving remarkable cost reductions of up to 40%. The question isn’t whether this transformation will happen—it’s whether your organization will lead or follow. The Current State: Why Manual Collections Are Failing The Human Agent Bottleneck Traditional collections operations are plagued by inefficiencies that seem almost archaic in today’s digital age. Human agents spend hours each day making outbound calls, often reaching voicemails, disconnected numbers, or unresponsive debtors. The average collections agent can only handle 50-80 accounts per day, with success rates hovering around 15-20% for first-contact resolutions. This manual approach creates several critical problems: Scalability Limitations: As portfolios grow, organizations must hire more agents, increasing overhead costs and training complexity. Each new hire requires weeks of training and months to reach full productivity. Inconsistent Messaging: Human agents, despite training, deliver inconsistent messages and may not always follow compliance protocols perfectly. This variability can lead to regulatory issues and damaged customer relationships. Limited Operating Hours: Traditional call centers operate during business hours, missing opportunities to connect with debtors who may only be available during evenings or weekends. High Operational Costs: Between salaries, benefits, training, technology, and facility costs, the total cost per agent can exceed $60,000 annually, not including the productivity losses from sick days, vacation time, and turnover. The Communication Gap Perhaps most critically, traditional collections methods fail to meet modern consumer communication preferences. Studies show that 75% of consumers prefer text-based communication over phone calls, yet most collections operations remain phone-centric. This disconnect creates friction that reduces payment rates and increases customer frustration. The AI Revolution: Transforming Collections Through Intelligent Automation Understanding AI Collections Bots AI collections bots represent a fundamental shift from reactive to proactive collections management. These sophisticated systems leverage natural language processing, machine learning, and integration capabilities to automate the entire collections workflow while maintaining personalization and compliance. Modern AI bots can analyze debtor profiles, payment histories, and behavioral patterns to craft personalized outreach strategies. They understand context, respond to objections, negotiate payment arrangements, and seamlessly escalate complex cases to human agents when necessary. The Power of Multi-Channel Integration The most successful AI collections implementations combine multiple communication channels with robust CRM integration: WhatsApp Business Integration: With over 2 billion users worldwide, WhatsApp has become the preferred communication channel for many consumers. AI bots can initiate conversations, send payment reminders, share payment links, and even process payments directly within the chat interface. Salesforce CRM Triggers: Integration with Salesforce enables sophisticated workflow automation. When specific conditions are met—such as a payment becoming 30 days overdue—the system automatically triggers personalized bot outreach sequences tailored to the debtor’s profile and history. SMS and Email Backup: For comprehensive coverage, AI bots can seamlessly switch between channels based on response rates and customer preferences, ensuring maximum engagement. Real-World Impact: The 40% Cost Reduction Reality Breaking Down the Cost Savings Organizations implementing AI collections bots report average cost reductions of 40%, but understanding where these savings come from reveals the true power of automation: Reduced Labor Costs (60% of savings): AI bots can handle the workload of multiple human agents simultaneously. A single bot can manage thousands of accounts, working 24/7 without breaks, sick days, or vacation time. Increased Collection Rates (25% of savings): By reaching debtors through their preferred communication channels at optimal times, AI bots often achieve higher contact and payment rates than traditional methods. Operational Efficiency (15% of savings): Automated workflows eliminate manual data entry, reduce processing time, and minimize errors, creating significant operational efficiencies. Case Study: Regional Credit Union Success A regional credit union with 50,000 members implemented an AI collections bot integrated with WhatsApp and Salesforce. Within six months, they achieved: 45% reduction in collections operational costs 35% increase in first-contact payment rates 60% reduction in accounts requiring human agent intervention 90% customer satisfaction rate with the bot interaction experience The bot handled over 10,000 collection cases monthly, with human agents focusing only on complex negotiations and legal proceedings. Building Your AI Collections Bot: A Strategic Framework Phase 1: Foundation and Planning Compliance First Approach: Before any technical development, ensure your AI bot framework complies with all relevant regulations including the Fair Debt Collection Practices Act (FDCPA), Telephone Consumer Protection Act (TCPA), and state-specific collection laws. Build compliance into the bot’s core logic, not as an afterthought. Data Integration Strategy: Successful AI collections bots require comprehensive data integration. Connect your existing systems including core banking platforms, loan management systems, payment processors, and customer databases to create a unified view of each debtor’s situation. Communication Channel Setup: Establish your multi-channel communication infrastructure. Set up WhatsApp Business API access, configure SMS gateways, and ensure email deliverability. Each channel requires specific setup and compliance considerations. Phase 2: Salesforce CRM Integration Trigger Configuration: Design sophisticated trigger rules within Salesforce that initiate bot sequences based on specific criteria such as: Days past due thresholds Payment amount and frequency patterns Previous contact history and responses Customer risk scores and segmentation Seasonal or economic factors Workflow Automation: Create automated workflows that update customer records, log interactions, schedule follow-ups, and escalate cases based on bot interactions. This integration ensures seamless handoffs between automated and human processes. Real-Time Sync: Implement real-time data synchronization between your bot platform and Salesforce to ensure agents have immediate access to all bot interactions when they need to intervene. Phase 3: AI Bot Development Natural Language Processing: Develop or integrate NLP capabilities that can understand customer responses, detect payment intent, identify hardship situations, and respond appropriately. The bot should handle common scenarios like payment confirmations, dispute notifications, and arrangement requests. Personalization Engine: Build dynamic message generation capabilities that personalize communications based on customer data, payment history, and previous interactions. Personalized messages consistently outperform generic templates. Payment Integration: Integrate secure payment processing directly

Salesforce Sales Cloud + Pardot Implementation